Roosevelt's Recession: A Historical and Econometric Examination of the Roots of the 1937 Recession

The Numbers Don’t Agree: A Review of Conflicting Studies

Throughout the decades, the 1937 Recession was of little interest to economists. Its predecessor, the Great Depression, is the focus of most of the related research. The varied recovery efforts that followed the Great Depression make it difficult to isolate and study and the causes of the Recession. Given the difficulty in studying this downturn, the little economic literature that exists has not reached a point of general consensus: it is split into three broad camps. Some texts contribute the downturn mainly to fiscal policy changes, some consider monetary policy shifts as the main cause, and some point to labor conditions as the culprit.

It took a decade after the Recession for serious, focused scholarship about it to appear. Kenneth D. Roose, a longtime economist at Oberlin College, was one of the earliest economists to devote much of his research to the study of the 1937 Recession. After completing his dissertation at Yale, titled “The Recession and Revival of 1937 - 1938,” he began expanding upon his research.122 In 1948, part of his dissertation was published in the Journal of Political Economy, and then in 1951 he published an article in The Journal of Finance, where he examined, more closely, the role played by net government contribution to income during the Recession. His research into the Recession culminated in 1954 when his book, The Economics of Recession and Revival: An Interpretation of 1937-38, was published. To this day, his book is the only book solely devoted to the study of this Recession.

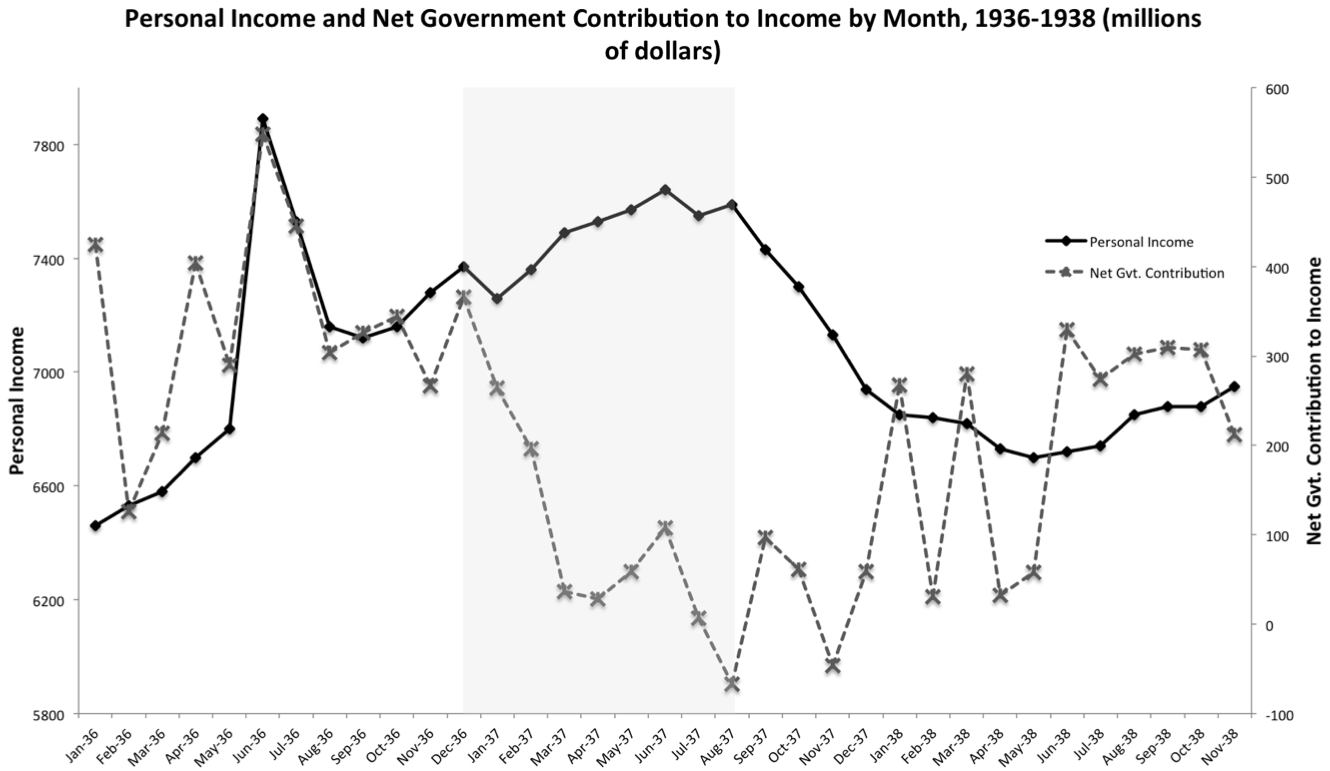

Roose’s 1951 paper is concerned with the role of fiscal policy in bringing about the Recession. From the onset, Roose declares that the decline in net government contribution to income, which he used as an indicator for the net effects of government expenditures and taxes, was a contributing factor to the Recession.123 His study seeks to examine not if, but how large of a role the decline of government spending played.Figure 5, adapted from Roose’s study, plots personal income and net government contribution to income between the years 1936 and 1938.124 As shown in the figure’s grey area, net government contribution to income began sharply declining in December 1936, yet personal income continued increasing without any significant decline for another nine months, until August 1937. Roose closely examined this significant lag to better understand the role of fiscal policy. He contends that the nine-month lag is so large that the decline in net government contribution to income "cannot be regarded as the principal immediate cause” of the decline in personal income.125 In other words, the downturn experienced in 1937 cannot be attributed solely to the decline in government spending.

Advertisement

Before examining the lagged effect further, consider the simultaneous peak of both line plots in the plot. Roose notes that “prices, production, and income rose rapidly” during the last few months of 1936.126 The $1.7 billion soldier’s bonus payment of June 1936 contributed to the expansion. In the next two months, nearly 71% of the total bonus payment was converted into cash. As the bonus is quickly converted to cash, the net government contribution to income graph declines to trend by September 1936, before fiscal policy tightening and expanded and new taxes sends the plot on a steep decline by December of that year. Therefore, the bonus payment, which was quickly converted to cash, had a sharp but brief impact on the economy. Any residual stimulating effects of the bonus payment on the economy should have disappeared by early Spring 1937.

{kind=link}

Figure 5. Personal income and net government contribution to income, 1936-1938. Refer to footnote number 124 for data source and variable definitions.

With the effects of the bonus payment ruled out, coupled with the steep decline in government spending since December 1936, personal income should have seen some decline by Spring 1937; however, it continued rising through August 1937. Given these two points, Roose argues that the only way the bonus payment could have contributed to the prolonged increase in personal income was by temporarily boosting business and consumer confidence. “Only in this very indirect sense, can it be argued that the bonus expenditures… contributed to the expansion of the level of income from January to June, 1937.”127

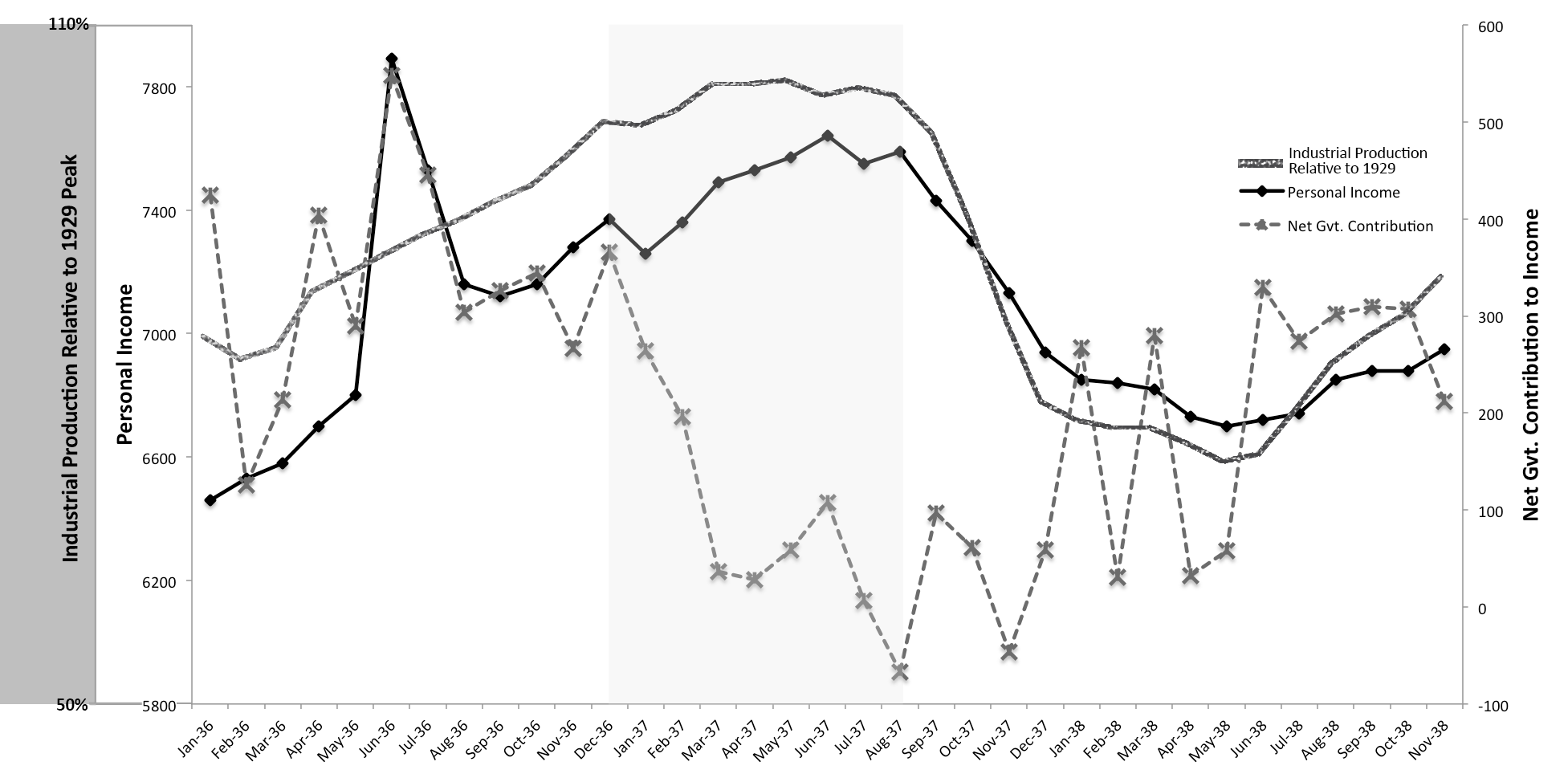

If we were to assume this is true, private industry was able to sustain the economy for over half a year after the decline in government spending. However, in the latter half of 1937, private industry was unable to offset the decline government spending.128 Both the personal income plot in Figure 5 and the industrial production index shown in Figure 2, show steep declines by August 1937. In Figure 6, industrial production is superimposed over Figure 5 to show the similar lagged decline seen in net government contribution and industrial production. Both measures are consistent and seem to fall in line with Roose’s point.

The inconsistent, large spikes in net government contribution to income point to an issue of timing. In regards to these wide fluctuations, Schumpeter commented, “Its high water mark came exactly at the time when the economic process could most easily have done without it and its cessation exactly at the time when the economic process was in its most sensitive phase.”129 Government too easily swayed its policy back and forth; the soldier’s bonus was rapidly dumped into the economy during a time of recovery, then spending was extremely and rapidly curtailed. There was a lack of moderation, which swayed the economy upwards, and then aided to its plunge without assistance.

{kind=link}

Given Roose’s points and findings, his study can be classified as pointing to fiscal policy as the cause of the Recession. The government adhered to strong pressures by the business community for balanced budgets by 1937. The continued expansion of the economy during the first half of 1937, as government expenditures were being curtailed, could have led many to believe that government was no longer needed for recovery. The latter half of 1937 proved otherwise: for whatever reason, private industry was unable to sustain growth. Pointing to fiscal policy contraction as the main cause, Marriner Eccles, in a radio address on January 23, 1939, declared the "rapid withdrawal of the governments stimulus was accompanied by other important factors… [and] the result was another period of rapid deflation in the fall of 1937, which continued until the present spending program of the government was begun last summer.”130

Friedman and Schwartz, in an often-cited passage, say, “The most notable feature of the revival after 1933 was not its rapidity but its incompleteness.”131 They point to a large gap in the recovery between nondurable industrial production and durable industrial production to underscore the low levels of private investment. In 1937, nondurables were 21% above 1929 levels, but durables were 6% below their 1929 peak.132 Friedman and Schwartz, in agreement with views put forward by Roose, argue that during this time, the lack of private investment was worsened by government policies that increased wages.

The Role of Wages

Advertisement

Having roughly established the untimely role played by government contributions to income, the focus is turned to wages. During his time in office, Roosevelt believed that the Depression was made worse by excessive competition, a sort of race to the bottom that reduced prices and wages.133 In adherence to this view, one goal of the New Deal was to increase prices and wages. To achieve this, the National Industrial Recovery Act (NIRA) was created in 1933 to limit competition in certain industries. Codes of competition were imposed on industries that agreed to raise wages and accept collective bargaining agreements. Most of the codes were comprised of trade agreements that curtailed competition, which included measures ranging from production caps to minimum prices.134 The expansive powers given to the Government under the NIRA led the Supreme Court to rule the act unconstitutional on May 27, 1935. Following the ruling, the National Labor Relations Act (NLRA) was enacted on July 05, 1935, with the same goal of increasing prices and wages.

One view put forward was that the Recession was caused by an increase in labor costs. The increased level of wages, which occurred in 1937 and was sharper than that caused by the NIRA, is attributed to the NLRA. The act, also known as the Wagner Act, addressed employer-employee relations and included a codified set of unfair labor practices.135 The constitutionality of the act was immediately challenged because of the new protections the act afforded employees and unions. It took two years for the Wagner Act to make its way through the judicial system. During this uncertain time period, the act had little effect on the economy. The constitutionality of the act, specifically the powers granted to the National Labor Relations Board, was argued before the Supreme Court on February 10-11, 1937. On April 12, 1937, in a 5-4 decision, the Court upheld the law.136 By early 1937, it became apparent that the Court would uphold the act, which impacted wages.

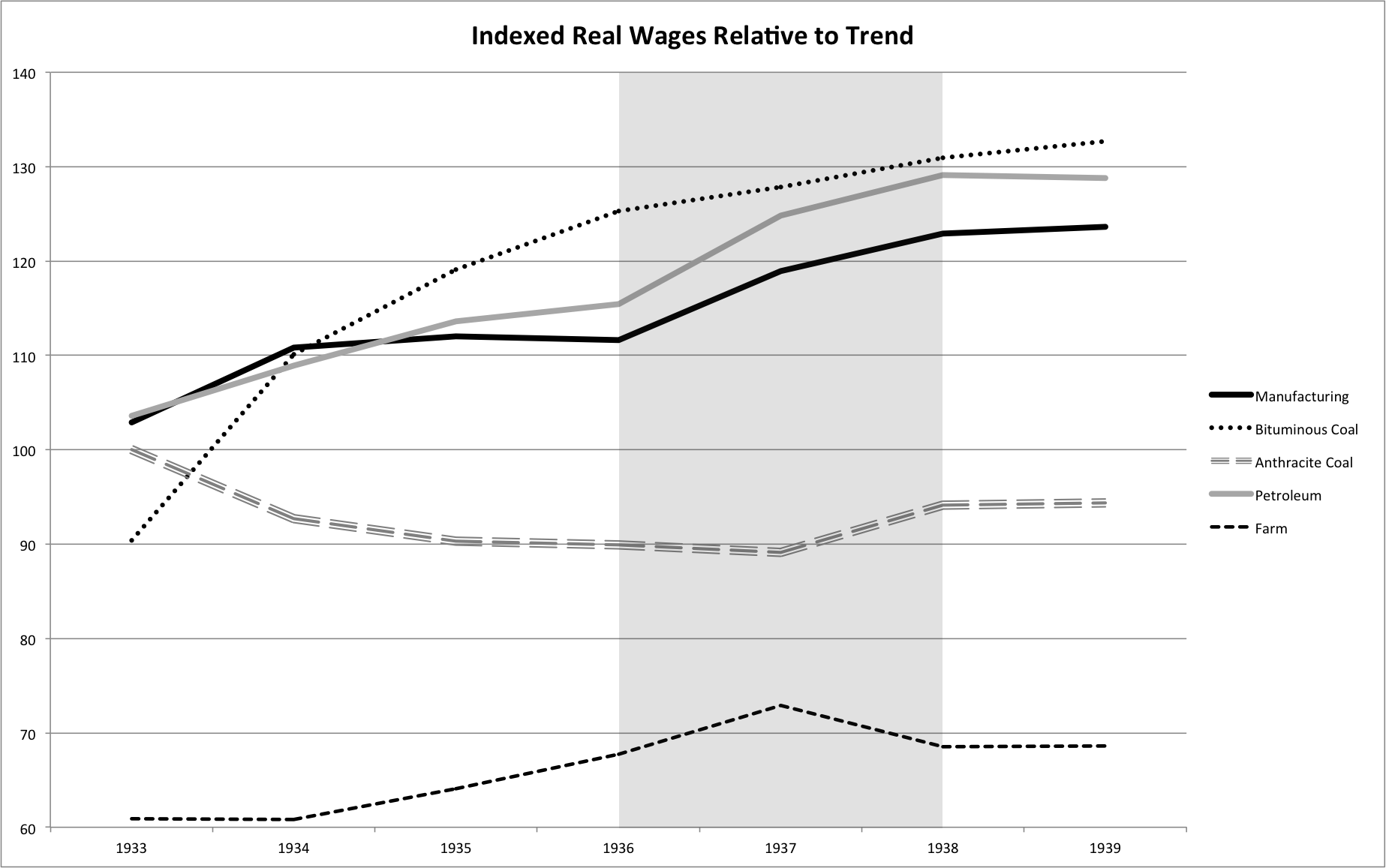

Figure 7 shows the 1937 spike in wages in certain key industries: manufacturing, bituminous coal, anthracite coal, petroleum, and farming. Real wages are indexed against a postwar manufacturing compensation growth rate of 1.4% and are deflated using the GNP deflator. Anthracite coal and petroleum is indexed to 100 for the year 1932, whereas all other industries are indexed to 100 for the year 1929. The use of this data allows for a more balanced comparison of wage trends across industries.

Of the five industries plotted, the farming sector is the only sector excluded by the NLRA collective bargaining and labor protections.137 As shown, the farming sector experiences no spike during the time period of interest. Similarly, the railroad sector, also exempted from NLRA protections, sees no increase in wages during this time.138

Of the four affected industries, only the bituminous coal sector maintains an upward trend that existed prior to 1936. The other three sectors, manufacturing, petroleum, and anthracite coal, experience significant and singular spikes in wage levels right around the time period that the NLRA was upheld. Between 1936 and 1938, de-trended real wages spiked 10% in the manufacturing sector, 4.5% in the bituminous coal sector, 4.7% in the anthracite coal sector, and 12% in the petroleum sector. It can be assumed that the NLRA had a significant impact on wages during the time period of focus. What remains to be proven, however, is whether the increase in the level of wages can be considered a cause of the 1937 Recession.

In testimony before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, Lee Ohanian, an economist affiliated with UCLA and the Hoover Institution, argued that the NLRA-induced wage increases "played a significant role in the 1937-38 economic contraction” because Roosevelt's cartel wage-setting measures distorted market forces.139 According to Ohanian, Roosevelt’s policies repressed employment and output in order to increase wages above market-clearing levels. True recovery, therefore, was prolonged by the distortion of market forces.

{kind=link}

Figure 7. Indexed wages relative to trend in five key sectors. Data adapted from: Cole and Ohanian, "New Deal Policies and the Persistence," 788.

Although it is clear that wages rose in response to the NLRA, many other economists discard Ohanian’s strong conclusion. Francois Velde, a senior economist and research advisor at the Federal Reserve Bank of Chicago, showed that Ohanian’s claim that higher-wages repressed employment is hard to prove. Velde regressed the percent change in employment against the percent change in average hourly earnings between September 1936 and November 1937 and found a negative relationship; a 1% increase in wages brought about a 1.8% fall in employment. Although, at the surface, these findings support Ohanian’s conclusion, Velde showed that the results are inconsistent and can easily vary based on the data used. For example, when he changed the end date by several months, from November 1937 to June 1937, his results changed drastically and were no longer significant at the 5% significance level.140 Velde showed that, although wage levels did increase in certain industries, it is hard to concretely relate an increase in the level of wages to a decrease in employment.

Christina Romer, one of the foremost scholars of the time period, also discounts the role played by an increase in the level of wages. Increased wages and unionization could have contributed to decreased output and investment: in other words, a supply shock. Romer argues that such a supply shock should have been followed by rising prices. However, producers’ prices actually fell by 9.4% during this time. In other words, wages did not have any significant negative impact on the economy because the theoretically required consequences of such a negative impact did not actually occur during the time period.141

Given the findings presented, coupled with the pronounced difficulty in pointing to wages as a cause, it can be assumed that wages played, at most, a minor role in the Recession. More important factors were at play.142

The Future and Public Perception

In an interesting and untraditional study, Eggertson and Pugsley examine the role played by muddled perceptions of the government’s future price objectives in bringing about the Recession. They argue that public confusion over future inflation targets led to changes in inflation and output, an effect that was amplified in the context of very low interest rates. Their paper rests on the notion that if the public believes in future contractionary policy, this belief creates actual expectations of contraction. However, at low interest rates, expansionary interest rate cutting cannot offset such expectations.143 They plainly state the following: “The mistake of 1937 was in essence a poor communication policy… confusing signals about future policy created pessimistic expectations of future growth and price inflation that fed into both an expected and an actual deflation.”144

Their paper examines the role played by monetary policy. Unlike those studies that examine the role of monetary policy before them, this study assumes the role of monetary policy is irrelevant at zero interest rates. It is not policy but expectations about policy that interests the authors. They say, “Our view is that the expectation channel straightens the argument… that monetary factors were responsible for the contraction of 1937-38.”145 Their paper builds on Eggertson's 2005 staff report, which was published in 2008; the paper credits post-1933 recovery to positive future expectations, as a result of Roosevelt’s policy promises.146 To test their argument regarding the 1937 slump, Eggertson and Pugsley first had to consider public perception of future policy decisions during the time period. In order to do this, they examined newspapers from 1937-1938.

By 1936, some within the administration believed the Depression was over.147 Roosevelt underscored this assumption in his annual message to Congress on January 6, 1937. In his address, Roosevelt called on Congress to continue enacting progressive policies in the interest of American society even though the Depression was over. He stated, “your task and mine is not ending with the end of the depression.”148 Such messaging about the end of the Depression was followed by government communication regarding an end of inflationary policies. Eggertson and Pugsley outline the progression of government anti-inflationary announcements, some of which are listed below:

- February 18, 1937: In a Senate hearing, Marriner Eccles expressed concern about low interest rates.

- March 17, 1937: The Secretary of Commerce and the Secretary of Agriculture hold a press conference and express concern about inflation.

- April 2, 1937: Roosevelt holds a press conference and expresses concern about inflation, specifically prices in certain markets.

- August 3, 1937: A letter between Roosevelt and Senator Elmer Thomas leaked. In the letter, Roosevelt rejects a proposal for a formal 1926 price-level target. 149

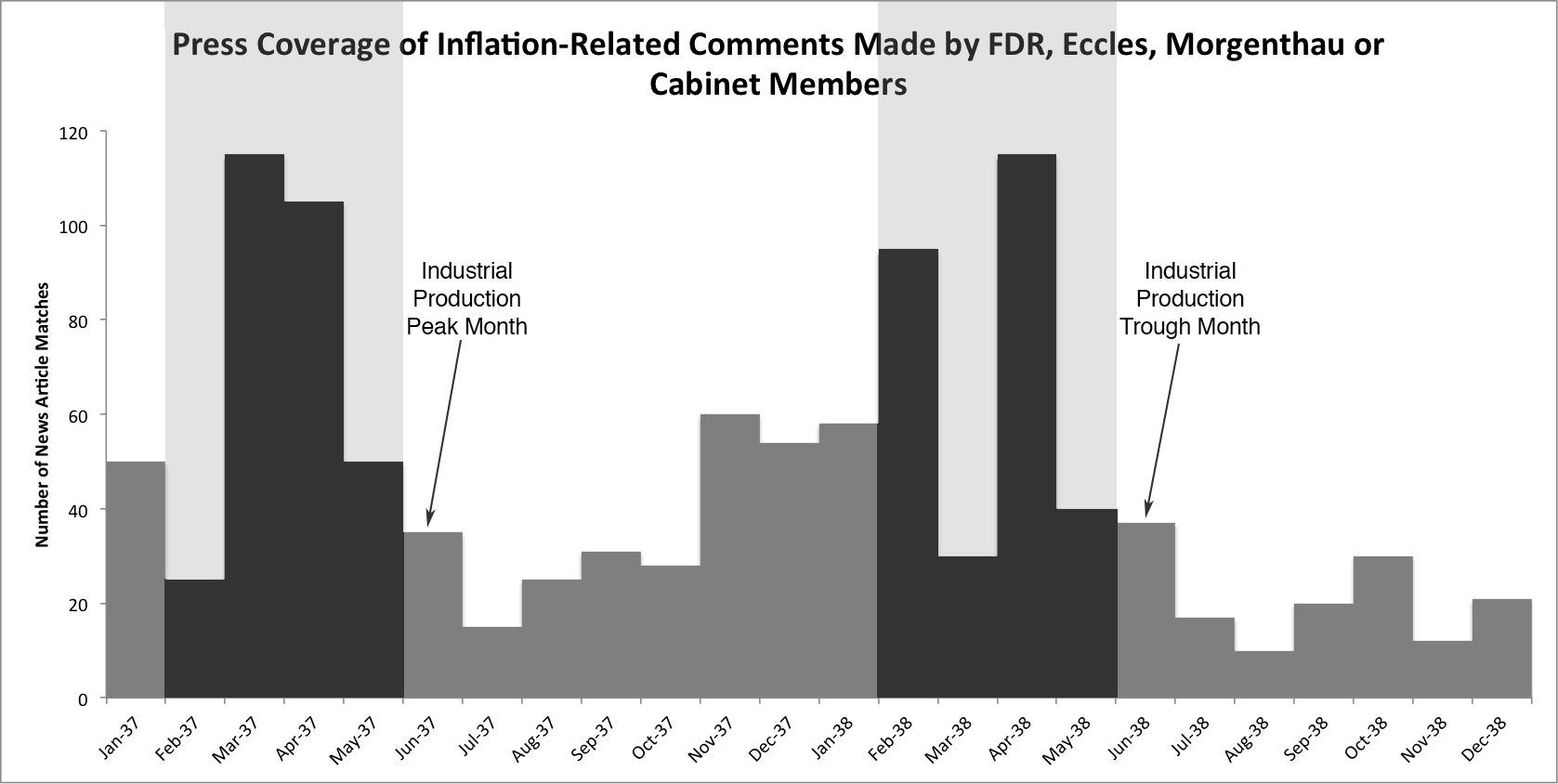

To more rigorously examine the role of public perception during the time period, Eggertson and Pugsley created an index to measure the intensity of inflation policy discussion. They used the Proquest Historical Newspaper database to search for articles that mention inflation, reflation, deflation, and price levels, while also including the name of at least one significant government official. Their index shows a very significant peak in inflation communication during the early months of 1937, before the onset of the Recession, and in early 1938, right before recovery.150 Their index value, treated as exogenous change in beliefs, is built into a model where industrial production is the output.

{kind=link}

Figure 8. Intensity of inflation-related press coverage. Data adapted from: Eggertsson and Pugsley, "The Mistake of 1937," 182.

Eggertson and Pugsley contend that, while their study provides a plausible understanding of why the Recession occurred, there were other contributing factors to the onset of the Recession. They assert their model is partly consistent with both the monetarist and the Keynesian interpretation of the Recession. In addition to monetary policy, they say, “Fiscal policy certainly played an important role, especially the efforts of the Treasury to balance the budget."151 The pulling back of fiscal policy fed into the public’s belief of an incoming deflationary regime. On both fiscal and monetary policy realms, the public was led to believe that deflation was on the horizon.

Having shown, through analysis of historical newspapers, that their theory fits the timeline of the downturn well, they continue their analysis and examine the recovery. Using the same methods, they show that the government began spreading pro-inflationary communication in the early months of 1938. The press widely reported on these communications, as shown by the large spike in inflation-related headlines in Figure 8 between January and April 1938. Aiding their conclusion is that the government, at the highest levels, seemed confused about proper policy steps. The President, completely reversing on his January 06, 1937 inflation warning, held a press conference on February 15, 1938, where he outlined his desire for inflation. In response to a question about price structures, the President stated that prices are “too low and ought to go up at the present time.”152

Surprisingly, the argument put forward by Eggerson and Pugsley seems to have a decades-long strand of agreement among economists with uncommon views. Friedman and Schwartz seem to agree, to some extent, that the Recession was partially caused by confusion and mixed expectations. Although they barely elaborate on the point because the bulk of their work is concerned with the Federal Reserve and reserve ratio requirements, Friedman and Schwartz quote Roose’s Economics of Recession to argue that “‘a bitter division of opinion over the New Deal, its measures and philosophy,’ hardly calculated to establish an atmosphere conducive to vigorous enterprise and confident risk taking.”153

A Quick Recovery

The recovery began as slowly as the Recession hit. Throughout the latter half of 1938, various economic indicators reached their minimum and began increasing. Some of these troughs are listed below by month.

- February: total and private construction contracts

- April: corporate bond prices, freight car loadings, nondurable consumer good production

- May: retail, department store, and chain store sales, mineral production, total imports, orders for manufactured goods, man-hours worked at manufactures of nondurable goods

- June: total income payments, total industrial production, man-hours worked in all manufacturing 154

The above list of various troughs indicates that recovery was on its way by Spring 1938, with the Recession coming to an end by June 1938. As Figure 2 helps show, a rebound began on June 1938. In the section of his paper concerned with the revival, Roose contends that revival from the Recession cannot be directly linked to an increase in government expenditure because numerous economic indicators “had begun to rise before the actual expansion in government spending” of June 1938.155 Roose’s section draws a weak, casual relationship between government spending and recovery due to timing; recovery began before June, but government expenditure expanded after May. In defense of Roose’s view, the net government contribution to income plot reaches an obviously prolonged high plateau beginning on June 1938; between June and November of 1938, the average government net contribution to income was $289 million. However, Roose’s argument is fundamentally flawed because he pays no attention to the fluctuations in net government contribution to income in the five-month time period before June.

Although government expenditures increased significantly after May, Roose fails to take into account the fluctuations during the five-month period, which when averaged, reach levels much higher than those seen in 1937. Between July and December 1937, the average contribution was $18.23 million, with the entire year’s average contribution being $66.75 million. From January 1938 to May 1938, the average contribution was $133.54; clearly, during the first five months of 1938, the level of net government contribution to income was much higher than that seen during 1937. Given these figures, Roose’s point regarding non-causality can be disregarded; net government contribution to income increased before, not after, signs of recovery trickled in. This shows, but does not prove, that government expenditures could have brought about the swift revival.Continued on Next Page »