Roosevelt's Recession: A Historical and Econometric Examination of the Roots of the 1937 Recession

2015, Vol. 7 No. 06 | pg. 1/8 | »

The 1937 Recession is a lesser-known event overshadowed by the Stock Market Crash of 1929 and the Great Depression. Nonetheless, it is a subject of deep interest because it brought about an uncommonly sharp economic downturn during the depression recovery period. A study of 1937 provides the unique opportunity to examine the casual contributing role, if any, of the historically unprecedented recovery efforts enacted by President Franklin Delano Roosevelt in 1933.

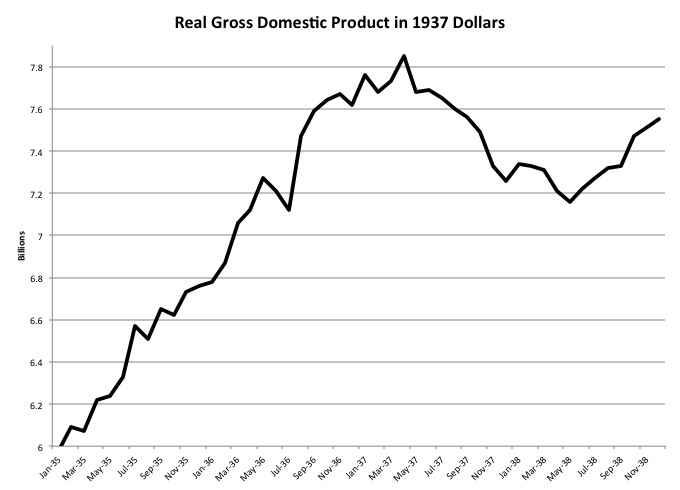

To set the stage, Figure 1 plots real gross domestic product (GDP) between the years 1935 and 1938.1 During the Recession, GDP declined nearly 10%.

{kind=link}

Figure 1. Real GDP in Chained 1937 Dollars. Source: The End of the Great Depression 1939-41, by Robert J. Gordon and Robert Krenn

Advertisement

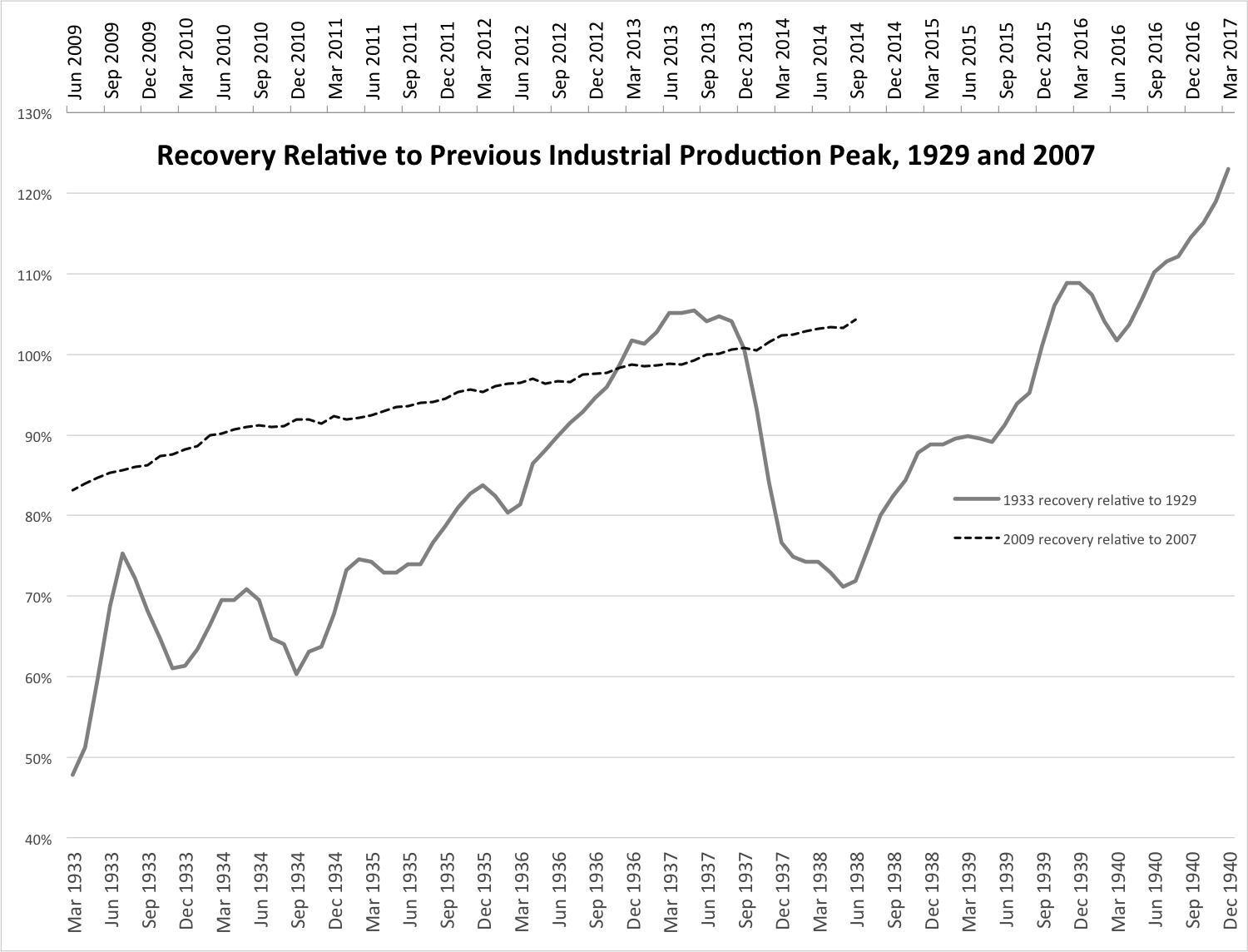

Industrial production output data allows for a more nuanced examination of the Recession’s impact. Figure 2 plots the NBER’s industrial production index, an indicator that measures the output of manufacturing, mining, and electric and gas utility production facilities. The solid grey line is a plot of the index between March 1933 and December 1940.2 The dashed line, provided for comparative purposes, plots industrial production during the 2008 Great Recession recovery period.

The years 1937 and 1938 should have been defined by continued recovery from the nation’s worst economic collapse. For reasons to be explored, overly optimistic policymakers and outspoken and disagreeing economists made key mistakes leading to the Recession. Confusion, a lack of theories, and ideological barriers jointly contributed to the downturn. A comprehensive understanding of society, politics, and economic thought during the decade prior to the Recession is required to understand the unprecedented and contested factors that contributed to its onset. The policymakers at the root of these factors made decisions that brought about one of the most unique downturns in American economic history.

___________

This study begins by turning the focus away from 1937 and gazing back to the onset of the Great Depression, starting with President Herbert Hoover’s time in office. Subsequently, this study examines the state of economic thought during the Recession and the development of new theories in response to the Great Depression. Finally, the project ends with a quantitative analysis that was recurrently complemented by the historical knowledge amassed.

Given that the varied recovery efforts that followed the Great Depression make it difficult to isolate the causes of the 1937 Recession, the little economic literature on this topic has yet to reach a point of general consensus. While some texts contribute the downturn only to fiscal policy changes, others consider monetary policy as the only cause. This study finds both views to be valid. Only in the context of diminished government spending was monetary policy able to have an impact great enough to lead to the Recession.

{kind=link}

Figure 2. Recovery Relative to Previous Peak, 1929 and 2007. Data adapted from: Board of Governors of the Federal Reserve System (US), Industrial Production Index [INDPRO] retrieved from FRED, Federal Reserve Bank of St. Louis.

The Crash and the Depression: A Nation, Surprised

Despite having gained the label of “do-nothing President” from his opponents across the aisle, President Hoover took a surprisingly proactive approach to addressing the alarming conditions that resulted from the Stock Market Crash of 1929. Hoover’s recovery efforts served as the foundation of President Roosevelt’s New Deal. Hoover "understood the importance of stimulating aggregate demand in a depressed economy and the economic policies he pressed for were intended for that purpose.”3 However, given his political philosophy and the social climate of the time, he believed that recovery required limited government intervention; he considered monetary policy as the only tool at his disposal. Rexford Tugwell, one of the architects of the New Deal, highlights the extent to which Hoover built the foundations for recovery by saying, “The ideas embodied in the New Deal legislation were a compilation of those which had come to maturity under Hoover’s aegis… all of us owed much to Hoover, [especially] for his enlargements of knowledge, for his encouragement to scholars, for his organization of research.” Tugwell continues, “The brains trust got much of its material from the Hoover committees or from work done under their auspices”4 Hoover’s dedication to research-backed policy decisions was a trait he brought to the White House from prior posts.

Before his time in the White House, Hoover served as the third Secretary of Commerce from 1921 to 1928. Although the position was considered one of the least prestigious cabinet posts, Hoover used his seat as a platform to advocate for issues outside of the traditional scope of his position.

During his first two years as Secretary, Hoover lobbied for restrictions on foreign lending. Hoover was concerned about the rise in foreign investment because he believed that “our citizens… have had but little experience in international investment.”5 Between the years 1924 and 1929, American foreign lending totaled $6.429 billion. During that same period, total British foreign lending was only $3.3 billion.6

The surge in foreign lending was the result of the 1913 Federal Reserve Act and financial sector ingenuity. Prior to the Federal Reserve Act, national banks in the United States were prohibited from opening branches abroad. The Act ended this prohibition, and the number of bank branches in foreign countries soared from 26 in 1914 to 181 in 1920.7 The new foreign branches gave international borrowers easier access to American lenders. In addition to international expansion, the increase in foreign investment was also tied to a financial instrument first introduced in 1921: the investment trust. Like the modern mutual fund, an investment trust pooled client contributions and invested the pooled fund on behalf of the clients. The use of the investment trust as a financial instrument started in Britain, where trusts traditionally invested in foreign bonds. When the instrument made its debut in the United States, the focus on foreign bonds was retained.8

Advertisement

Responding to the increases in foreign investment, Secretary Hoover ordered the Commerce Department to assess foreign investments. With the new mandate, the Department provided economic condition summaries and investment project information to hundreds of U.S. banks.9 However, the assessments did little to alleviate Hoover’s concerns. Even during his Presidency, Hoover was worried about over-investment, both nationally and abroad. Unlike many of his contemporaries, he believed that the market was overvalued.10

As President, Hoover felt it was pertinent to caution the public about the dubious increase in market values. In early 1929, he instructed Treasury Secretary Andrew Mellon to provide the public with investment advice. Following Hoover’s directive, on March 14, 1929, Mellon made a public statement encouraging investors to look beyond corporate stocks. Mellon announced, “The present situation in the financial market offers an opportunity for the prudent investor to buy bonds,” and he pointedly continued, “bonds are low in price compared to stocks.”11

An aspect central to Hoover’s concern about the market was the method underlying the expansion in stock purchases. As stock values inflated, and as more Americans flocked to the market in hopes of earning easy money, the financing of stock purchases became commonplace. Individuals willing to take out a loan could now easily invest more than they would otherwise have been able to afford. By September 1929, outstanding broker’s loans obtained by NYSE members totaled $8.5 billion. The value of loans outstanding had nearly doubled in less than two years.12 Figure 3 shows the rise in the value of broker’s loans outstanding.

{kind=link}

For comparison to modern day amounts, the value of outstanding broker’s loans in 1928 represented the value of 8% of 1929 GDP. To relate these numbers to values today, 8% of GDP in 2014 represents $1.28 trillion.13 As these figures show, the value of broker’s loans outstanding in the year 1929 was an extraordinarily high amount. As time will tell, the vast amount of money tied up in these un-discountable and risky loans contributed, in part, to a banking crisis that brought the financial system to its knees.

It is important to note that concern over security speculation had long existed outside of the President Hoover’s office. In its annual report for the year 1923, the Federal Reserve Board discussed, at length, recommended credit policy. The discussion underscored the importance of “productive,” or non-speculative, uses of credit. The Board warned that a speculation in commodity stocks could produce disequilibrium between production and consumption:

The characteristic of the good functioning of the credit system is to be found in the promptness and in the degree with which the flow of credit adapts itself to the orderly flow of goods in industry and trade. So long as this flow is not interrupted by speculative interference there is little likelihood of the abuse of credit supplied by the Federal reserve banks and consequently little danger of the undue creation of new credit...It is the nonproductive use of credit that breeds unwarranted increase in the volume of credit; it also gives rise to unnecessary maladjustment between the volume of production and the volume of consumption, and is followed by price and other economic disturbances.14

However, it took the Federal Reserve Board half a decade to apply their 1923 speculation doctrine. It wasn’t until their 1929 report that the Board devoted significant discussion to the rampant security speculation.15 A contemporary student of economics may be surprised to discover that, before the 1929 crash, opinion was sharply divided among economists and policymakers about the nature of stock prices. The disagreement regarding speculation is best highlighted in an infamous address given by Irving Fisher, a renowned economist and leading figure in the field. On October 15, 1929, during a speech in New York City before the Purchasing Agents Association, Fisher assured audience members and other stakeholders that, despite what others are saying, stocks have reached "what looks like a permanently high plateau.”16 Fisher’s prediction stood the test of time for less than ten days.

The Stock Market Crash of 1929 is considered by most to be the start of the Depression. However, some economists believe that the crash should not have had an impact outside of the stock market. Milton Friedman, in an interview for Newsweek in 1970, simply stated, “Whatever happens to the stock market, it cannot lead to a great depression unless it produces or is accompanied by a monetary collapse.”17

Friedman’s statement in Newsweek reflects the conclusion that he and Anna Schwartz reached in their groundbreaking and contested 1963 book, A Monetary History of the United States, 1867-1960. Chapter Seven of their book, “The Great Contraction,” argues that the 1929 stock market crash would not have led to a downturn as long and as painful as the Great Depression had the Federal Reserve not presided over a contraction of the money supply.18 They state, “The monetary collapse was not the inescapable consequence of other forces, but a largely independent factor which exerted a powerful influence on the course of events.”19

A series of banking crises between 1930 and 1933 brought about the collapse of the financial system. Given the structure of the American banking system, bank failures and bank runs occurred with regular frequency in the decades before the Depression. Bank failures were often hyper-local events that affected small banks in rural areas. However, the three banking crises that occurred between 1930 and 1933 were unprecedented due to their sequential timing and the large sum of currency held by the suspended banks.

The first baking crisis began during October of 1930 and tapered off in early 1931. During this period, bank failures peaked in November and December. In November, 256 banks, with total deposits of $180 million, failed. The following month ushered in the failure of 352 banks, with total deposits of over $370 million.20 The deposits of suspended banks in November 1930 alone were more than double the previously recorded maximum, since the onset of monthly data recording in 1921. The most dramatic of the bank failures during the first crisis was the collapse of the Bank of United States on December 11, 1930. With over $200 million in deposits amongst its 440,000 depositors, the failure of this New York City-based bank represented the largest commercial bank failure, as measured by deposits, in American history.21 22

Just months after the stock market crash, towards the end of the first banking crisis, economists and policymakers predicted the onset of recovery. Upticks in certain economic indicators led many to conclude that the worst had passed. James A. Farrell, President of U.S. Steel, proclaimed in January 1931, “The peak of the depression passed thirty days ago.”23 In the first few months of 1931, industrial production rose, and factory employment was declining at a lower rate.24 However, these slight upticks weren’t enough to increase public confidence. The total value of deposits in suspended banks started increasing after March 1931: a second banking crisis was unfolding.Continued on Next Page »